ARTICLES

Plan for the Spending after Retirement

Retirement is a time to relax and enjoy the fruits of your labour, but it's also when your income may significantly reduce. In addition, the global trend of increasing life expectancy cannot be ignored. Take Japan, for instance, where recent statistics reveal that women and men have an average life expectancy of around 84 years and 80 years, respectively. It means one would probably spend more years without work-related income than before. That's why it's essential to start saving for retirement early to ensure financial security during these extended post-work years.

Making Retirement Plan: Things to Consider

How much do you need?

There is no standard answer to this question. It will depend on your lifestyle and expenses. A good rule of thumb is to aim at replacing 70-80% of your pre-retirement income with portfolio withdrawals, pensions and other sources of non-work-related income.

Example:

Alice earns $50,000 a month before retirement. She may target at least $35,000 a month from various sources. If she retires at 65 and expects to live to 80, she will need $35,000 x 12 x (80 – 65) = $6,300,000 for her retirement fund.

How much time do you have before your targeted retirement age?

The earlier you begin saving, the more time your money has to grow and take advantage of the powerful force of compound growth. Over an extended period, this compounding effect can create a snowball effect.

Example:

Alice, Becky and Cathy each start with a principal of $50,000 in a savings plan that offers a fixed annual interest rate of 5%. They contribute $500 per month, but their journeys differ as they start at different ages. Alice initiates her savings plan at the beginning of her 31, Becky at 41 and Cathy at 51. Now, let's fast forward to their retirement, at the end of their 65 and see what happens*:

| Total Years in the Plan |

Total Contributions | Total Interest | Total Balance | |

|---|---|---|---|---|

| Alice | 35 | $50,000 + 35 x 12 x $500 = $260,000.00 | $557,722.61 | $811,722.61 |

| Becky | 25 | $50,000 + 25 x 12 x $500 = $200,000.00 | $255,680.34 | $455,680.34 |

| Cathy | 15 | $50,000 + 15 x 12 x $500= $140,000 | $93,417.79 | $233,417.79 |

What's truly remarkable is that Becky and Alice contributed around 43% and 86% more than Cathy, respectively. Yet, their total plan balances turn out to be over 195% and 347% more than Cathy's. This scenario beautifully illustrates the power of compounding. As the interest earned each year is added to the principal, the principal itself grows, leading to higher interest. Over a prolonged period, this compounding effect can lead to an exponential growth of your savings.

So, remember, starting early can make a world of difference. Don't underestimate the potential of time and the snowball effect it can have on your financial future.

What kind of retirement lifestyle do you envision?

Retirement often brings new opportunities and desires, such as increased travel or indulgence in luxury experiences. For instance, while you may have opted for budget flights and hostels in your younger years, you might prefer first-class flights and upscale accommodations after leaving the workforce, which come with higher costs. These choices can significantly impact your travel budget.

Similarly, as you enter retirement, you may have more time to explore hobbies and interests. While some hobbies have minimal costs, such as hiking or reading, others, like learning wine tasting or pursuing certain artistic endeavours, can involve higher expenses for classes, materials or equipment. It's important to consider the potential financial implications of these hobbies when planning for retirement.

Additionally, you may want to expand your social network by joining volunteer activities. Again, different volunteering opportunities can vary in cost. Engaging in local community volunteering may have a minimal financial impact, but if you aspire to participate in overseas volunteer programmes, it's essential to factor in these costs as well.

By considering these potential lifestyle changes and their associated costs, you can better align your retirement savings and financial preparations with the lifestyle you desire.

Other considerations

There are other factors to consider when planning for retirement. One crucial aspect is the potential for a longer lifespan. People are living longer than ever before, which means you may need to sustain your retirement savings for a longer period. It's essential to account for this extended timeframe and the associated costs, particularly healthcare expenses. Healthcare costs are rising and accessing healthcare services may become more expensive as you age. As ageing populations grow, it's also wise to anticipate potential delays in accessing public healthcare or consider budgeting for private healthcare options.

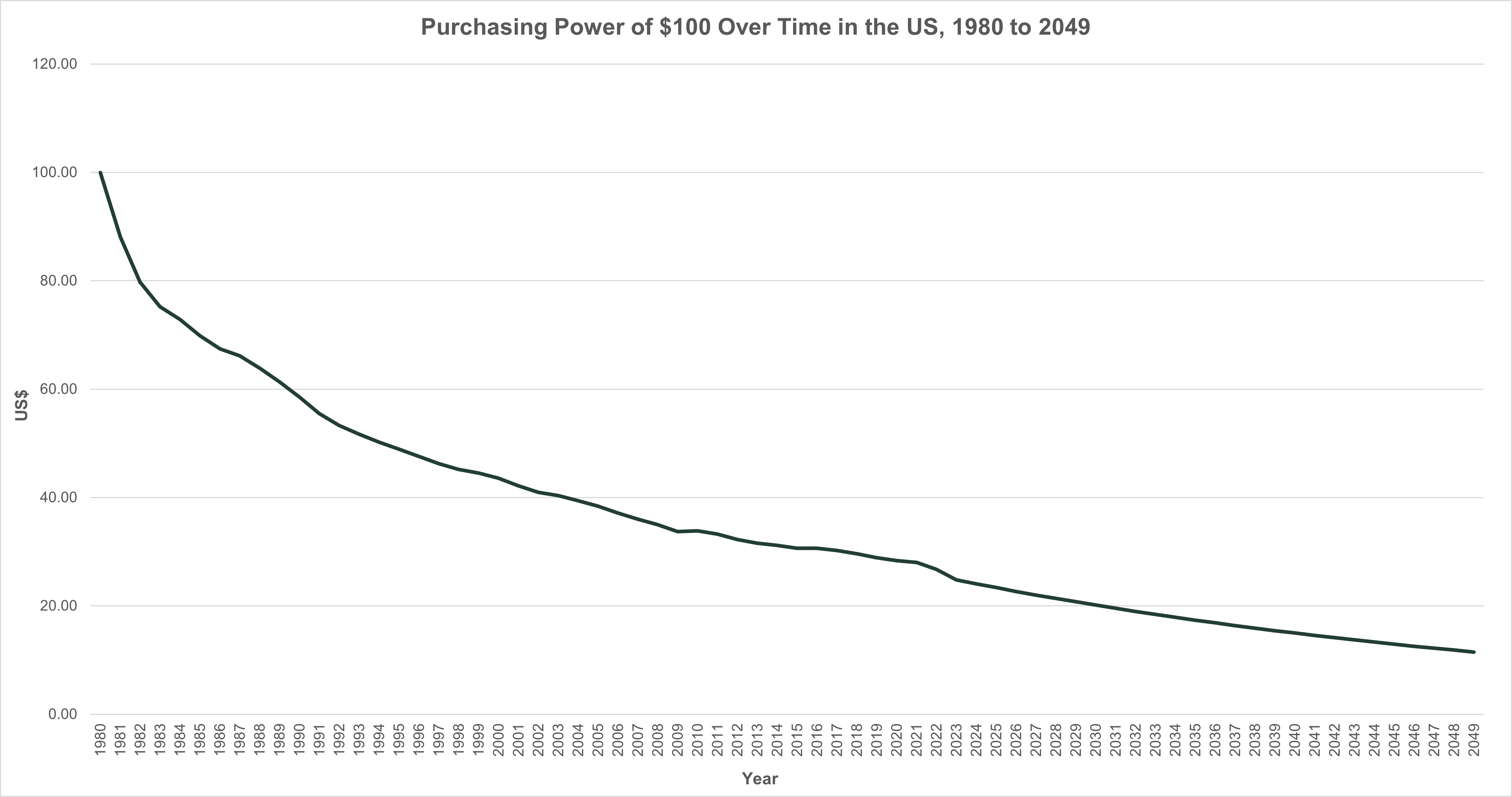

Another factor to keep in mind is the impact of inflation. Consider the following scenario.

Scenario:

You were given a US$100 note when you were born in 1980. In 1980, it could be used to buy US$100 worth of items. Based on the historic inflation rates in the US from 1980 to 2022** and assuming a future inflation rate of 3% per year, how much will the US$100 note be worth in terms of purchasing power in 2049, after 70 years?

The answer is US$11.5!

The scenario shows the value of money decreases due to inflation over time, which can erode the purchasing power of your savings. Therefore, it’s crucial to invest your money wisely in assets that have the potential to outpace inflation.

In conclusion, effective retirement planning allows you the freedom to choose the type of retirement lifestyle you desire, whether simple or luxurious. By taking the necessary steps early on, you can ensure that financial concerns don't hinder your ability to enjoy your retirement years. Act proactively to set yourself up for a comfortable and secure retirement. If you are unsure of what to do, don’t hesitate to seek professional advice who can tailor a plan that meets your individual needs.